Corporate bonds in volatile markets

How to make the most of fixed income

Corporate bonds have typically been a useful diversifier from the supposedly riskier equities, as they provide a reliable source of income, and are theoretically less volatile.

But are they worth investing in now?

Corporate bonds are issued by companies, and if fears are mounting that we are about to enter more volatile times, especially post-Brexit, then there may be more economic volatility for the companies issuing the bonds.

There is certainly demand for more investment into corporate bonds, from investors looking for a safe haven

However, years of low interest rates and central banks' asset purchases have meant that bonds are now low-yielding assets, and have taken on some of the risk profile of equities.

Here we outline some of the pros and cons of corporate bond investing.

Almost two thirds of advisers (63 per cent) believe that corporate bonds will not protect investors’ capital from the volatility in the stock markets right now, according to the latest FTAdviser Talking Point Poll.

Alistair Cunningham director at Wingate Financial Planning said he believed repositioning a portfolio to be more heavily in corporate bonds solely to protect against volatility was unwise.

He added: “Corporate bonds are a useful diversifier to sit alongside equities but any perceived protection is only theoretical, and in some investment markets may not work.

“The credit crunch in 2008-2009 is a good example where both of the main asset classes fell at the same time.

“Losses are inclined to be temporary in any case, so it’s more important an investor has the stomach to withstand dread scenarios as well as the financial capacity to weather any downturn – invariably the worst thing that can happen is to sell out in a declining market.”

Government bonds are often seen as the most defensive area of the bond market and therefore have arguably the more defensive classes so are likely to better protect investors if concerns over the market or economic outlook are significantly higher.

Adrian Lowcock head of personal investing at Willis Owen said corporate bonds in this situation would be less defensive as there was always the risk that a business could go under in a deep recession, as even the bond prices of financially stable businesses can suffer during a downturn.

He added: “Corporate bonds might appeal if the interest rate spread between them and government bonds widen so the yield of corporates remains higher relative to government bonds.

“This effectively means that investors are getting rewarded with a yield for taking on the risk of investing in corporate bonds and will be better protected should sentiment shift and become more positive.”

“The market is in a holding pattern, the next phase for the global economy is not clear with sentiment and expectation changing on the latest piece of data.

“In this climate, the equity and bond markets can swing as investors switch from risk-on, to a risk-off attitude, which means whether you invest in shares or bonds you could end up on the wrong side of sentiment and for bond investors this could be painful if the economic outlook improves, volatility stops and the equity market starts to perform.

“The best approach in the current climate is to have exposure to strategic bond funds as these have the flexibility to invest across the whole market.”

Do corporate bonds offer diversification in volatile markets?

Words: Fiona Nicolson

Pictures: Fotoware

Corporate bonds have typically been a go-to diversifier against the volatility of the equities market – especially in periods of uncertainty.

And according to Morningstar data published in their fund flows commentary, at the end of October, investors are continuing to find them useful, in these turbulent times, indicating that they are perceived to be a safer bet.

Morningstar’s figures showed that global corporate bonds received £436m worth of net inflows in September, up from the £279m allocated to corporate bonds in the previous month.

Fixed income as a whole drew the highest net inflows in September (£583m), further emphasising that investors are looking for what they believe to be a ‘safe haven’.

Why are corporate bonds in demand?

The demand for corporate bonds, and more broadly fixed income as a whole, can be attributed to a number of factors relating to seeking ‘safety’.

An ageing population...and the slowdown in economic growth are increasing the demand for fixed income

The current and potential impact of Brexit and its outcome is inevitably in the picture, but there is more to it than that, as Andrey Kuznetsov, senior portfolio manager at Hermes Investment Management points out.

He says: “An ageing population, the current geopolitical environment and the slowdown in economic growth are increasing the demand for fixed income − there is high demand for investment-grade and high-yield corporate bonds, which have seen consistent inflows this year.”

The approach taken by central banks is key too, as Mr Kuznetsov adds: “The accommodative central-bank stance has been a major contributor – for instance, the 180 degree turn by the Federal Reserve, from interest-rate hikes, to interest-rate cuts, has also led to demand from investors.”

Corporate bonds, while perceived as a safer haven, are of course not risk-free.

Robin Kyle, an investment expert at Scottish Widows emphasises that there is no such thing as certainty for investors: “I wouldn’t call corporate bonds a safe haven; they’re a lower-risk asset class.”

I wouldn’t call corporate bonds a safe haven; they’re a lower-risk asset class

A similar point is made by Edward Park, deputy chief investment officer at Brooks Macdonald Asset Management, who says: “Investment grade bonds are not risk free − the sterling investment-grade spread is around 1.5 per cent over gilts at the moment with a duration of around eight years.

“This spread is effectively the payment for taking on the additional risk of a corporate over a gilt and moves depending on the perceived credit and liquidity risk of the bond.”

But they undoubtedly have their attractions at the moment, as Ben Deane, an investment specialist in the fixed-income team at Fidelity International points out: “Investment-grade corporate bonds have got high-quality issuers, reducing risk of default. They also have stable cashflows and good forecasts.”

And as Paola Binns, senior fund manager at Royal London Investment Management points out, corporate bonds fulfil a need, as she explains: “We continue to see inflows into our corporate-bond funds, which suggests that investors need fixed income.”

Corporate bond performance

So, are corporate bonds rewarding investors with strong performance?

The answer is a resounding yes, according to Armando Lopez, head of fixed income at Santander Asset Management: “Corporate bonds are performing very well, supported by the low interest-rate environment and the reopening of the asset-purchasing programme by the European Central Bank.”

Others share his opinion: “This year has been a stellar year for corporate bonds,” says Mr. Deane.

Central banks have been much more accommodating than they were in Q4 last year, when they were tightening

“As at the beginning of November, investment-grade credit has been delivering a return of 7 per cent to 12 per cent.

“Central banks have been much more accommodating than they were in Q4 last year, when they were tightening – it is a more supportive environment for high-quality corporate bonds.”

Mr. Kyle also describes corporate bonds’ performance as outstanding, as he states: “Year-to-date, corporate bonds have significantly outstripped UK equities.

“For bonds to outstrip equities over the period of one year is a stellar performance.”

And some have stood out in particular, as Ms. Binns reports: “Corporate bonds have performed very well, especially those with long maturities – the over 15-year index has given a return close to 20 per cent year to date.

“Longer-dated corporate-bond funds have performed best, due to falls in interest rates, as well as improved pricing for corporate debt.

“Short-dated corporates have not done as well, but returns have been much better than cash.”

There are a number of reasons why corporate bonds have turned in a positive performance this year.

These include duration and what are perceived as potential glimmers of light at the end of the tunnel, with regard to Brexit.

Corporate bonds have benefited from their duration features, which worked very well over the summer

Reflecting on some of the contributing factors, Charles Younes, research manager at FE Investments says: “Corporate bonds have benefited from their duration features, which worked very well over the summer when yields reached historic lows.

“They also did well at the beginning of the year, as investors were keen on taking risk.”

Brexit can perhaps also take some credit for a rebound, when looking at which corporate bonds are thriving in the current climate, as Ms. Binns adds: “UK risk corporate bonds have performed exceptionally well recently, after being subdued since the beginning of the year, due to Brexit concerns.

“Recent developments have been taken as positive by the markets.”

A dimming of the light?

While corporate bond performance has been positive, there have also been some changes to watch out for, according to financial planner, Mel Kenny, of Radcliffe and Newlands, who observes: “Although this asset class has traditionally been known as a provider of income, corporate bonds have been behaving like equities of late, with less and less return from income.

“This increases their risk and questions their reputation as a natural diversifier.”

Another financial planner, and director at Rowley Turton in Leicester, Scott Gallacher is also staying prepared for change: “We’re cautious on this sector – we want to be able to move in and out of corporate bonds quickly, if need be.”

Reflecting on bond funds as a whole, Jeff Keen, head of fixed income at Waverton Investment Management says: “We think that bond funds will need to be much more dynamic and flexible in order to generate returns which are attractive for investors.

“We doubt that many bond funds are well-equipped for the next phase of the bond cycle, which we anticipate will be extremely challenging.

We doubt that many bond funds are well-equipped for the next phase of the bond cycle

“Bond funds need to be of a size which matches the current liquidity constraints in bond markets – that is, they should avoid being very large bond funds – and need the ability to use derivatives to hedge out duration and/or credit risks when appropriate.

“We fear that there is a huge amount of money invested in bonds as a cash alternative, at a time when interest rates are at historic lows.

“For many years, bonds have delivered an impressive profile of cash plus returns. When that changes, we expect those strong flows to reverse, and we doubt that the bond market is set up to absorb that selling appetite.”

Mr. Park is also cautious about corporate bonds, as he explains: “We reduced our exposure to corporate bonds earlier in the year driven by two things: concerns about liquidity in the asset class and a desire for the purer defensive exposure of shorter dated gilts.

“We have a slight overweight to equity risk compared to our strategic benchmark, therefore in order to balance that risk we have reduced our exposure to investment grade bonds due to their sensitivity to the movement of credit spreads.

What should clients look for in a corporate bond fund?

So, what should clients look for in corporate bonds, to achieve their investment goals?

Mr. Deane believes it comes down to a few specific points, as he explains: “The three things clients should be looking for from corporate bonds are income, diversification from equities and minimising volatility. When we’re constructing client portfolios, this is our focus.”

He adds: “We have a bias towards defensives, for instance utilities and are cautious on financials, like banks, as they are more volatile and have a higher correlation to equities.

“We also want a healthy balance of duration and credit, as duration is what gives us diversification from equities.”

Mr Deane also takes the view that clients should prioritise liquidity when it comes to corporate-bond funds: “Liquidity is of particular relevance at the moment, so investors should make sure that their managers are positioning their portfolio accordingly.

“Our approach is to create a healthy balance, including some gilts and supranationals, and we make sure any illiquidity is compensated for in spread terms.”

There are other areas that clients should take note of with regard to corporate-bond funds, as Mr. Kyle suggests: “While it’s been a period of stellar returns for corporate bonds, there is no such thing as a free lunch.

“There’s been a huge flow into high-yield bonds and if there are a few bankruptcies, there could be a collapse.

“Clients should make sure that their portfolios are being sensibly managed and diversified by geography and credit. Investors should be looking for good diversification, sensible credits and where possible, exposure to high-quality issuers.”

And when it comes to selecting which corporate bonds, BB and BBB-rated bonds may be the better choice, says Mr. Kyle: “It used to be that people would go all the way down to junk bonds, but it’s not worth the risk any more.

“BB and BBB-rated bonds have been the ‘sweet spot’ for the last three years. Any lower and investors are not being compensated for the additional risk.

“If a CCC-rated bond were to default, for example, there likely wouldn’t be anything left to distribute to bondholders.

“The most attractive opportunities are in good companies that can cope with slowing economic growth.

“Many managers are lending for longer to these companies, to help generate a pick-up in yield, now that duration, (interest-rate) risk has reduced.”

House View: Some inconvenient truths about income

“Chin up. Be positive. It’ll all work out.”

We are always being encouraged to look on the bright side, but too much optimism can be dangerous.

Take the simple matter of how much we expect to earn from our savings and investments.

We are always being encouraged to look on the bright side, but too much optimism can be dangerous.

Far too many people around the globe take a “glass half full” approach to future returns that simply does not match reality.

The truth is, we live in a world where record low interest rates and years of asset purchases by central banks have led to record low bond yields.

That means that when we put money away in the lower-risk investments and savings accounts that helped the previous generation save for retirement, the returns we are seeing are simply not enough to grow our money.

This situation seems unlikely to change any time soon.

Even central banks that had been raising interest rates, like the US Federal Reserve, have changed tack this year and are now cutting rates again.

Despite this, when Schroders surveyed 30,000 people worldwide, we found that irrational optimism is rising.

Average expectations of annual investment returns over the next five years now stand at 10.7 per cent – nearly one percentage point higher than at the same time the year before.

This optimism is mirrored the world over: investors in the Americas anticipate annual returns of 12.4 per cent; in Asia they expect 11.5 per cent and in Europe the expectation is for 9 per cent annual returns over the next five years.

Financial advisers might dream of such returns, but they certainly would not dare to predict them.

So why do savers and investors believe returns will be so high?

And, more importantly, why does it matter?

The problem of recent history

It is often said that investors have short memories and our study confirms this.

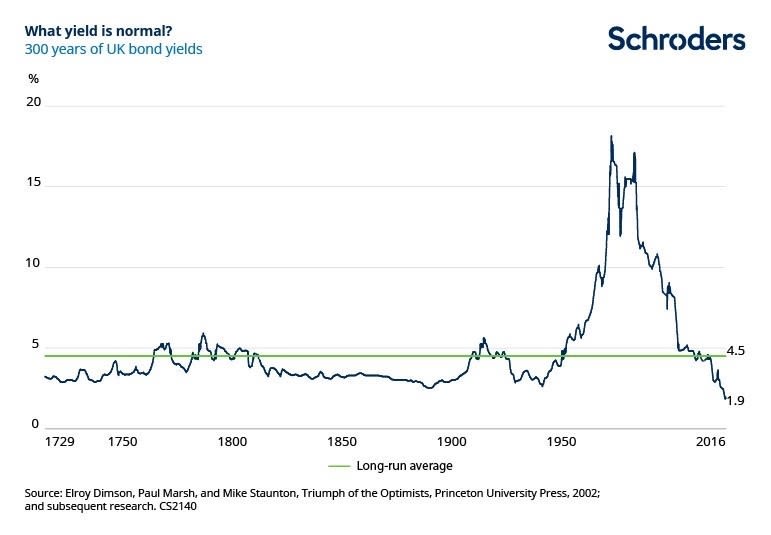

Specifically, investors and savers around the globe seem able to remember only back to the 1970s, 1980s and 1990s, when interest rates and bond yields looked very different to how they are now.

Those were the days when my father could put money into an National Savings & Investment bond, backed by the British government, and gain a 15 per centrisk-free return.

Savers in many countries could live off the income from their savings accounts.

These double-digit returns for savers have become stuck in our memories.

However, they were the exception, not the rule.

Across a broader sweep of history, bond yields have stayed far closer to where we are today, as the chart below shows.

Returns for savers were correspondingly lower too.

The first inconvenient truth is this: high interest rates were a historic anomaly – they will not return soon.

More unpalatable facts

Further truths about the future of the global economy support our view that the returns investors expect will be hard to achieve.

The global labour force is declining, thanks to lower fertility rates, and this will contribute to slowing growth.

Productivity growth is also expected to slow, even in emerging markets.

The era of “catch up” growth as they closed the gap with the developed world is ending.

Then there is the ageing population, a much-discussed problem that will put pressure on government finances worldwide and compound the effects of slower population growth.

Across the world, the picture for growth is gloomy. Every economically important region is expected to experience lower GDP growth over the next ten years than the average since 1996.

Emerging markets will increase their share of global GDP, with China becoming particularly critical to the world economy.

But even the Chinese tiger faces threats. Its policymakers will have to deal with its own demographic changes for its economy to flourish.

Finally, inflation, which could drive investment returns, is expected to be muted by decreased demand and the deflationary impact of new technology.

The net result of all of this will be a low return, low interest rate environment that looks very different from the 10.7 per cent returns over-exuberant investors expect.

Solutions for a half-empty glass

Why am I telling you your glass is half empty?

Because having unrealistic expectations does nobody any favours, especially now that so many of us are being asked to put our own financial plans in place to fund our old age.

Accepting that we have entered a low and slow income environment is the first step.

Not only do you have something to plan for, you also have choices about how to tackle the gap between those expected high returns and the probable lower reality.

One obvious step that can be taken is to invest more, and to invest sooner.

The miracle of compounding will then ensure the possibility of greater returns over the long run. If you can put more money away now, it will make a big difference.

Another solution is to step up the risk you take.

Higher risk equities may produce higher returns, but you must be comfortable with your level of risk and understand the potential volatility this may cause along the way.

And in a low-income environment, skilled active managers can really make a difference.

Diversified funds, picked by those who understand the global economic realities we face, can ensure that your money works as hard as possible for you while it is invested.

Pick a fund that works for you. Then your glass really could be (more than) half full.

Rupert Rucker is head of income solutions at Schroders

Bank your CPD